The Fight Over the City's Flood Zones Will Matter for Years to Come

Shortly after Sandy, then-Mayor Michael Bloomberg complained that the flood zones which dictated who needed to buy flood insurance were too small. Sandy, city officials said at the time, proved as much, since the storm damaged thousands of homes that were located well outside the official 100-year flood zone.

Now the de Blasio administration officials say the feds have gone too far. They say the new zones are threatening to make working-class neighborhoods like Canarsie in Brooklyn and Howard Beach in Queens unaffordable.

“That has real implications for neighborhoods, homeowners and residents because it’s going to drastically increase flood insurance premiums,” said Dan Zarilli, the city director of the city’s Office of Resiliency and Recovery. “It could price people out of their homes in a really bad way.”

FEMA’s flood maps predict which parts of the country have a 1 percent chance of being flooded in any particular year – the 100-year-flood. Property owners inside the zone generally are required to buy flood insurance to qualify for a federally backed mortgage, an expense that could cost thousands of dollars of year. And if a developer wants to construct a new home or building in the zone, the maps say how high the builder must place the first habitable floor.

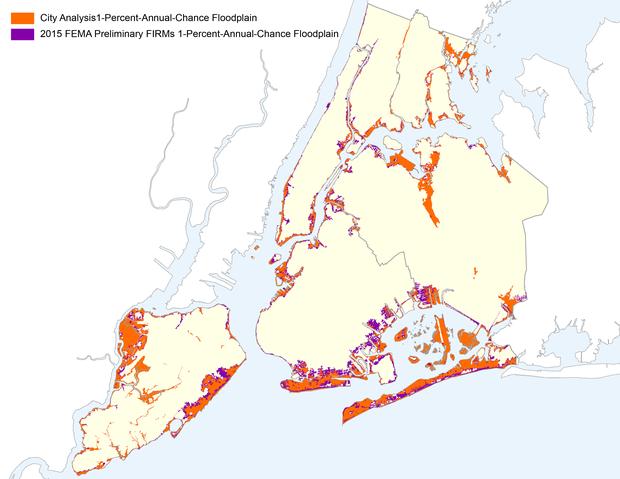

In a process that began before Sandy but did not conclude until after the storm, FEMA issued a proposal for new maps that doubled the size of the flood zone, saying better technology and science led to a more reliable conclusions.

Because of the high stakes, the city hired an engineering firm last year that analyzed FEMA's methodology. In an appeal to FEMA filed last week, the city argued that FEMA's flood zone is really 35 percent larger than it should be, and will affect 170,000 people unnecessarily. The appeal was first reported in the Daily News.

Philip Orton, an oceanographer at Stevens Institute of Technology, separately evaluated the proposed flood zones and agreed that FEMA exaggerated the size of the 100-year-flood zone.

“In their whole assessment, there is one storm that was dramatically worse than all the others, in November 1950,” Orton said. “And when we went back and looked at whether or not they reproduced the storm correctly, we found that the flood height was dramatically overestimated.”

But shrinking the zones has its own drawbacks. New homes may not be built high enough off the ground, and if a lot of property owners don't buy flood insurance even though they need it, that means taxpayers will once again get stuck with the bill when a big storm comes.

“It's strange to see New York City asserting that they over-predict the risk of flooding,” said Rob Moore,a senior policy analyst at the Natural Resources Defense Council.

For one, FEMA did not look at any storm from the past decade, when sea levels have risen two or three inches and when three of the top 10 high-water events of the past 100 years occurred (Sandy, Hurricane Irene and a March 2010 Nor’easter). And the maps also do not anticipate any sea level rise in the future, while experts suggest as much as 30 inches could be added over the next three decades.

A representative from FEMA, Andrew Martin, said that the agency would consider the appeal and issue final flood zone maps in the near future. The earliest those maps would take effect, however, would be 2016.

WNYC is funded by sponsors and member donations